Intel Announces Q4 2017 and FY 2017 Results

by Brett Howse on January 25, 2018 10:55 PM EST- Posted in

- CPUs

- Intel

- Financial Results

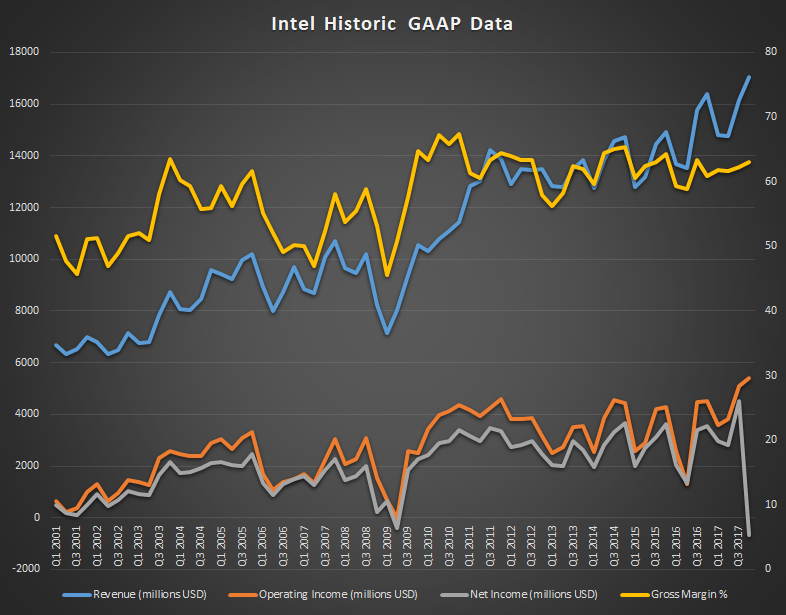

Today Intel announced their quarterly earnings, and 2017 was another record year for the company. Q4 revenue was a record $17.1 billion, and the full year revenue was a record $62.8 billion. For this quarter, Intel’s GAAP earnings took a hit due to a $5.4 billion tax expense thanks to the new tax reforms that were enacted in December, but as a one-time hit, it shouldn’t be a concern going forward. In fact, Intel is forecasting only a 14% tax rate for FY 2018.

In GAAP terms, Intel’s gross margin was 63.1%, which is up 1.4% from a year ago, and their operating income was up 19% to $5.4 billion. However, thanks to a 111.4% effective tax rate due to the one time $5.4 billion tax fee, Intel is actually reporting a GAAP loss for the quarter of $0.7 billion. Earnings per share were therefore down 120% to a loss per share of $0.15.

Due to the tax impact, it’s probably a good thing to look at Non-GAAP earnings as well which will exclude that one-time charge. In terms of Non-GAAP, Intel’s gross margin was 64.8%, which was up 1.7%. Operating income was up 21% to $5.9 billion. Intel’s Non-GAAP tax rate was 21.2%, which is actually higher than the 19.8% they paid last year, and net income was $5.2 billion, up 34% from a year ago. This led to earnings per share being up 37% to $1.08.

For the full year, Intel had $62.8 billion in revenue, with a gross margin of 62.3%. Operating income was up 39% year-over-year to $17.9 billion, although thanks to the tax hit their net income was down 7% to $9.6 billion. In Non-GAAP terms, net income was up 27% to $16.8 billion.

| Intel Q3 2017 Financial Results (GAAP) | |||||

| Q4'2017 | Q3'2017 | Q4'2016 | |||

| Revenue | $17.1B | $16.1B | $16.4B | ||

| Operating Income | $5.4B | $5.1B | $4.5B | ||

| Net Income | -$0.7B | $4.5B | $3.6B | ||

| Gross Margin | 63.1% | 62.3% | 61.7% | ||

| Client Computing Group Revenue | $9.0B | +1.6% | -2.0% | ||

| Data Center Group Revenue | $5.6B | +14.7% | +20.0% | ||

| Internet of Things Revenue | $879M | +3.5% | +21.0% | ||

| Non-Volatile Memory Solutions Group | $889M | -0.2% | +9.0% | ||

| Programmable Solutions Group | $568M | +21.1% | +35.0% | ||

Intel is still pivoting business away from the declining PC market, and they have done well to diversify, but still, their PC business is still the biggest piece of the pie. For the quarter, the Client Computing Group had revenues of $9.0 billion, which is down 2% year-over-year, but for the full year of 2017, their CCG was up 3% to $34 billion. It’s not quite dead yet. In an effort to show their diversification, Intel is now quoting their data in “PC-centric” and “Data-centric” and conveniently, Data-centric is all of their business outside of the CCG, but even so, the CCG still accounted for 53% of Intel’s revenue for the quarter.

But, the Data-centric group is certainly growing much quicker than the PC market which is still in a decline. The Data Center Group is by far the largest portion of Intel’s Data-centric efforts, and the DCG had revenues of $5.6 billion for the quarter, which are up 20% year-over-year. With the expansion of the cloud, this likely still has some ways to go before it hits a peak, so it’s likely just a matter of time before they finally surpass their Client Computing Group.

The rest of the Data-centric business was also up for the quarter, with IoT up 20% year-over-year, to $879 million. For the full year the IoT was up 20% and had revenues of $3.2 billion. Non-volatile memory was up 9% for the quarter to $889 million, and for the year it was up 37% to $3.5 billion. Programmable Solutions was up 35% for the quarter to $568 million, and for the full year, was up 14% to $1.9 billion.

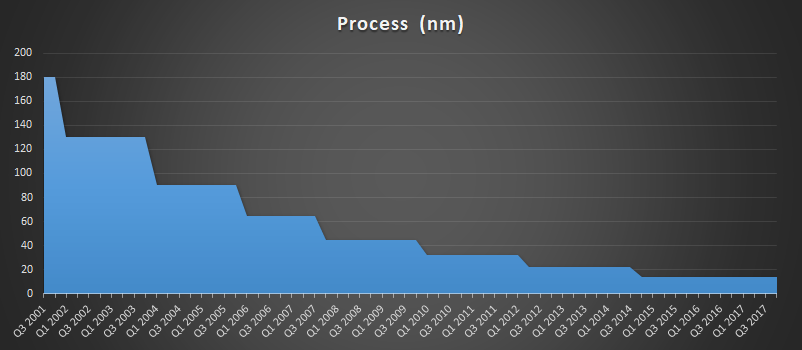

Intel still hasn’t shipped anything on 10nm to the point where someone could go buy a chip, although we’re finally getting close, with Intel shipping 10nm to some of their partners. 14nm was delayed, but the delay in getting to 10nm has been longer than likely anyone expected. Intel has still made some bold claims about density, so it should be a good node for them if and when it arrives.

Intel’s forecast for Q1 2018 is for $15.0 billion in revenue, plus or minus $500 million, and despite the rough start to 2018, they are still forecasting another record year, with $65 billion in revenue, plus or minus $1.0 billion.

Source: Intel Investor Relations

42 Comments

View All Comments

Tkan215 - Friday, January 26, 2018 - link

This company is a joke. This quarter doesnt reflect what is coming next. Intel already mention fallout that mean more things falling apart. No big companies want to have one company monopoly the whole data center in the world. Amd already stealing pc pie from intel othwrwise their pc sales should be much higher than reported. Their research and development is lower i wonder how they would compete.HStewart - Friday, January 26, 2018 - link

And AMD is has re-organization because of fallout from departure of Raju. AMD market is like a spec of sand to Intel.Samus - Saturday, January 27, 2018 - link

Could change since their server class and workstation CPU’s EPYC and Threadripper aren’t affected by Meltdown, outperform Intel for the price, and use less power.Probably explains why vendors can’t keep them in stock since they’ve been released.

woggs - Friday, January 26, 2018 - link

Yep... Intel is a $17B, 63% margin "joke" in Q4. Pretty funny joke, dude. A joke for... what? 30 years now?? Are you even that old yet? The stock market resoundingly disagreed with you today, too.serendip - Sunday, January 28, 2018 - link

You're right about the data center comment. Google, Microsoft, Facebook etc. are in the data business so they don't care what hardware they use, as long as it meets a price/performance figure. I'm typing this on an ARM mobile platform while my x86 tablet sits unused most of the time. Intel has the inertia of x86 support to keep it in business but the future looks increasingly heterogenous with multiple hardware platforms performing more specialized tasks.And all running Linux, of course ;)

Alistair - Friday, January 26, 2018 - link

The most interesting thing to me is that it basically didn't cost Intel any money at all to offer us 4 cores instead of 2, and 6 instead of 4.Their margins are so important, they didn't offer a huge easy increase in speed for years. I've had no sense for a few years that my money given to Intel has any effect whatsoever on their future product improvements.

Compare with how you feel when you buy a Tesla etc. or support a company that is striving to make better versions of what you love (Nintendo for example).

serendip - Sunday, January 28, 2018 - link

It's the marketing "geniuses" that run Intel now. They're the ones who can segment white sandwich bread into a million categories just because they can. Intel was so scared of cannibalizing their own sales (is self-cannibalism a thing?) that they let their tech go out in dribbles. It was only when AMD showed them Ryzen that they jumped off their behinds. Having a monopoly isn't a good thing in the long run.Hurr Durr - Sunday, January 28, 2018 - link

You're a bona fide retard if you buy a Tesla.Pork@III - Saturday, January 27, 2018 - link

delaying is demonstration of long sexual expiriencepoohbear - Saturday, January 27, 2018 - link

this is still the only major semiconductor and tech stock that didnt double in the last 3 years. what's up with that? even MS doubled. Nvidia alone is 12 times their 2014 valuations, and AMD went from $2-$17