SK Hynix to Buy Intel’s NAND Memory Business For $9 Billion

by Ryan Smith on October 20, 2020 9:30 AM EST

In a joint press release issued early this morning, SK Hynix and Intel have announced that Intel will be selling the entirety of its NAND memory business to SK Hynix. The deal, which values Intel’s NAND holdings at $9 billion, will see the company transfer over the NAND business in two parts, with SK Hynix eventually acquiring all IP, facilities, and personnel related to Intel’s NAND efforts. Notably, however, Intel is not selling their overarching Non-Volatile Memory Solutions Group; instead the company will be holding on to their Optane memory technology as they continue to develop and sell that technology.

Per the terms of the unusual agreement, SK Hynix will be acquiring Intel’s NAND memory business in two parts, with the deal not expected to completely close until March of 2025. Under the first phase, which will take place in 2021 once all relevant regulatory bodies have approved the seal, SK Hynix will pay Intel the first $7 billion for their SSD business and Intel’s sole NAND fab in Dalian, China. This will see Intel’s consumer and enterprise SSD businesses transferred to SK Hynix, along with the relevant IP and employees for the SSD business, but not any NAND IP or employees. Similarly, while SK Hynix will get the Dalian fab, the first phase does not come with the employees that operate it.

Following the first phase, Intel will continue to develop and manufacture NAND out of the Dalian fab for roughly the next four years. This period is set to last until the rest of the deal fully closes in March of 2025. At that point, SK Hynix will pay Intel $2 billion for the rest of their NAND business. This will finally transfer all of Intel’s NAND IP and related employees over to SK Hynix, along with the Dalian fab employees. Intel and SK Hynix have not offered any explanation for the prolonged acquisition, so we’re hoping to find out a bit more with the companies’ relevant earnings calls this week.

Meanwhile, Intel will continue to hold on to their Optane memory business. Optane is considered a “platform differentiator” by the company, as Intel intends to continue leveraging the technology for their unique, high-capacity NV-DIMMs. Accordingly, Intel has announced that they will be continuing to develop the underlying 3D XPoint technology and sell products based on it, which is consistent with their long-term aspirations of making Optane its own tier in the memory/storage hierarchy.

Overall, selling off their NAND business is a big step for Intel, a company that started out making memory. But it’s not entirely unexpected, as Intel has never been quite as successful with their NAND business as they would have liked. And the core of the company’s NAND efforts, their longstanding IMFT joint-venture with Micron, started winding down in 2018 when the two companies announced that they would stop jointly developing flash memory.

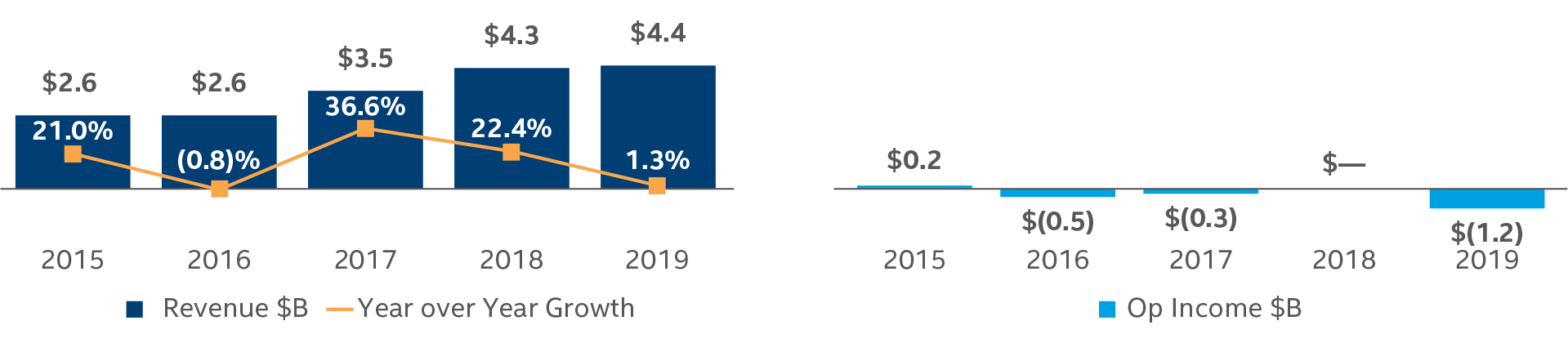

Since then, Intel has largely been walking its own path, securing the #5 spot in the NAND industry (generally right behind #4 SK Hynix) and releasing new products, but struggling with the commodity nature of the NAND business. While Intel’s Non-Volatile Memory Solutions Group (NSG) as a whole brought in $4.4B in revenue for 2019, the group has lost money for 4 of the last 5 years, recording flat or negative operating incomes. Only in the last six months has Intel made any real money off of NAND, reporting $600M in operating income for the first half of 2020. So although NSG – and by large part, Intel’s NAND business – have played a big part in Intel’s record revenues, they haven’t turned a significant profit for a company that’s renowned for their 60% gross margins.

Intel NSG Revenue and Operating Income, 2015-2019

Meanwhile for SK Hynix, the Intel deal opens the door to some new opportunities, and it also helps formerly fourth-place company company scale up to deal with the competition of its three remaining rivals, Samsung, Kioxia/WD, and Micron. TrendForce estimates that once this deal closes, SK Hynix will become the second-largest vendor of NAND, with over 20% market share, placing it behind market leader (and rival Korean firm) Samsung. Like many other commodity component markets, the NAND flash market has been subject to wild swings in profitability and the resulting pressure to consolidate, so by picking up Intel’s NAND business, SK Hynix will be in a stronger position going forward.

But the real pearl for SK Hynix is Intel’s enterprise SSD business, which the company specifically calls out in its joint press release. Despite its overall modest size, Intel’s NAND business has a major presence in the enterprise SSD market thanks to its early investment there as well as its domination of enterprise CPU sales. Intel’s chief (and arguably only serious) competitor in this space has been Samsung, so acquiring Intel’s SSD business makes SK Hynix that much more capable of going toe-to-toe with their biggest rival.

Intel Enterprise "Ruler" SSDs

Long term, however, it remains to be seen what SK Hynix will do with the NAND fab side of Intel’s business. While it’s clear that they have big plans for SSDs and intend to leverage Intel’s existing market share and customer relationships – which is a big part of why they’re acquiring that segment first – SK Hynix doesn’t necessarily need Intel’s NAND manufacturing technology. SK Hynix is plenty capable of building more fabs on its own if it wanted more raw NAND capacity, and indeed the company has undergone several expansions. Meanwhile the companies’ technologies are significantly different, as Intel relies on floating gate tech while SK Hynix uses charge trap tech. So although the two technologies have their trade-offs, it’s very questionable whether SK Hynix wants to continue developing both over the long run.

And for both parties, the long run really is the key. NAND flash is still facing a likely dead-end in the long run, as NAND has been scaled down almost as small as it can go before leakage becomes a serious problem. 3D NAND stacking has given NAND a second wind in the interim, but there’s only so far that can go, especially in respect to reducing bit costs. Which is a big part of the reason why Intel developed 3D XPoint to begin with, as the technology doesn’t suffer the same scalability restrictions. So although Intel is getting out of the NAND game, they are still very much in the storage game over the long run, now focused on a non-volatile memory technology that is expected to scale much further in the future.

Speaking of the future, Intel has also stated that they will be investing the expected proceeds from the sale into some of their other non-core, forward-looking businesses. Intel’s 5G, AI, and edge efforts are all slated to benefit from the sale, and all are markets that Intel is priming for potentially extreme growth over the coming years.

In the interim, however, the next step will be up to regulators. SK Hynix’s acquisition will need the approval of American, South Korean, and Chinese regulators, which the companies expect to take around a year – and at which point SK Hynix can start the actual acquisition. Meanwhile Intel is set to announce its Q3 earnings this Thursday, at which point we may hear a bit more about the deal from Intel’s perspective. SK Hynix’s own earnings call will follow in a couple of weeks, on November 3rd.

Source: SK Hynix & Intel

64 Comments

View All Comments

lmcd - Tuesday, October 20, 2020 - link

Yea imo there's assuredly room for yield improvements if nothing else. Also I'm sure controller optimizations could be huge for the space -- once NAND generations stabilize, controllers can be more directly designed for NAND performance profiles (re: SK Hynix's own P31).Rictorhell - Tuesday, October 20, 2020 - link

Very excited for this, IF it means more affordable higher capacity consumer SSDs in the somewhat near-term. I would even be thrilled with some "miraculous" SK Hynix capacity breakthrough, after acquiring all of Intel's research and patents, that allowed them to double or triple current maximum consumer SSD capacities. *a guy can dream*Billy Tallis - Tuesday, October 20, 2020 - link

To be fair, Intel has already been doing a good job of marketing their QLC to consumers at competitive prices. (That's now their entire consumer SSD strategy, since they stated earlier this year that they were not going to do any more consumer TLC drives.) So even if Intel held on to their NAND business, we could expect the upcoming 144L QLC and future generations to hit the consumer market in follow-ups to the 660p and 665p.Getting more options for consumer SSDs beyond 2TB is less a matter of technology right now than a matter of needing drive vendors willing to bring niche models to market. Sabrent seems to have helped break the ice a bit there, and now we're seeing other Phison partners launch 4TB or 8TB options.

nunya112 - Tuesday, October 20, 2020 - link

a fair few moves happening here. So intel and Micron have a pretty sweet relationship.and now Intel has sold its NAND business... That opens up a lot of questions for me . as to why get rid of a business that is really profitable.

Intel cant be hurting that bad for cash?? whats the real reason here????

Cullinaire - Tuesday, October 20, 2020 - link

did you even read the article? The division was hardly a fountain of profits for the past 5 years.PandaBear - Friday, October 30, 2020 - link

Intel NAND / SSD were falling behind in capacity, I think the money is in the 4-16TB SSD in enterprise right now and Intel is hardly catching up above 4TB, basically selling old stuff at the moment, and will get worse soon.Eliadbu - Wednesday, October 21, 2020 - link

To be honest, deal of that sort was long overdue. Intel fab buissnes is not competitive nor it has substantial revenue, while other player could use it to leverage it own business in the long run.rasheed - Wednesday, October 21, 2020 - link

5 years is a big time, this deal may not go throughYojimbo - Thursday, October 22, 2020 - link

$7 billion will be paid soon, in 2021 if I remember. The remaining $2 billion is to be paid in 2025. That makes it very likely the deal with go through, I believe, because SK Hynix is unlikely to walk away when they've alresdy paid over 3/4 the cost and Intel likely doesn't have an option to change their mind. I guess there could be something in the agreement about sending the $7 billion back, but I doubt companies pass $7 billion back and forth very often.Yojimbo - Thursday, October 22, 2020 - link

I read the details of the deal here in this article. Seems Intel keeps the NAND IP and operates the fab until 2025. The deal is strange because Intel has little incentive to develop technology they are exiting and which they've already sold for a fixed price in the future. Plus Intel's NAND technology is different from the rest of the industry's includubg SK Hynix. I would guess that SK Hynix will change the fab over to charge trap when it takes it over.The 4 year period might be a way to get the maximum value of Intel's IP roadmap before it's sunsetted. A good deal of R&D that Intel has already done will probably be applicable 4 years out, after which it will peter out unless new foundational research is pursued starting now, which no one will now do since Intel is exiting the business. Since SK Hynix does not have the expertise in Intel's technology and isn't interested in it, Intel will manage the development and manufacture of the NAND that goes into the product lines SK Hynix is buying from Intel.