Intel Reports Q3 2020 Earnings: Still Very Profitable, But Challenging Times Ahead

by Ryan Smith on October 22, 2020 9:00 PM EST- Posted in

- CPUs

- Intel

- Financial Results

Once again kicking off our earnings season coverage for the tech industry is Intel, who reported their Q3 2020 financial results this afternoon. The traditional leader of the pack in more than one way, Intel has been under more intense scrutiny as of late, particularly due to their previously disclosed delay in their 7nm manufacturing schedule. None the less, Intel has been posting record revenues and profits in recent quarters – even with a global pandemic going on – which has been keeping Intel in good shape. It’s only now, with Q3 behind them, that Intel is starting to feel the pinch of market shifts and technical debt – and even then the company is still well into the black.

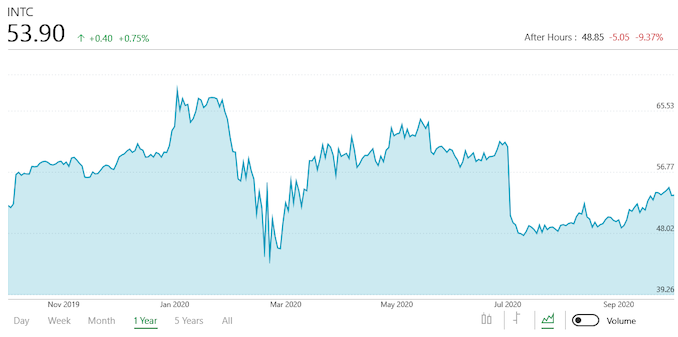

For the third quarter of 2020, Intel reported $18.3B in revenue. A drop of $0.9B over the year-ago quarter. As previously mentioned, Intel has been setting a string of record revenues in previous quarters, but the boom is coming to an end as margins and revenues are slipping. Those declines are also having the expected knock-on effect to Intel’s profitability, with the company reporting $4.3B in net income, a 29% drop versus Q3’19.

This also marks the second quarter where Intel’s overall gross margin has been noticeably soft. The company, normally known for its zeal for 60% margins, recorded a margin of just 53.1% for Q3, following last quarter’s 53.3%, and 58.9% a year ago. The drop in gross margins is a big part of Intel’s financial story for the most recent quarter: according to the company, average selling prices (ASPs) are down as customers gravitate towards cheaper products, and meanwhile costs are up as Intel further ramps up its 10nm plans.

| Intel Q3 2020 Financial Results (GAAP) | |||||

| Q3'2020 | Q2'2020 | Q3'2019 | |||

| Revenue | $18.3B | $19.7B | $19.2B | ||

| Operating Income | $5.1B | $5.7B | $6.4B | ||

| Net Income | $4.3B | $5.1B | $6.0B | ||

| Gross Margin | 53.1% | 53.3% | 58.9% | ||

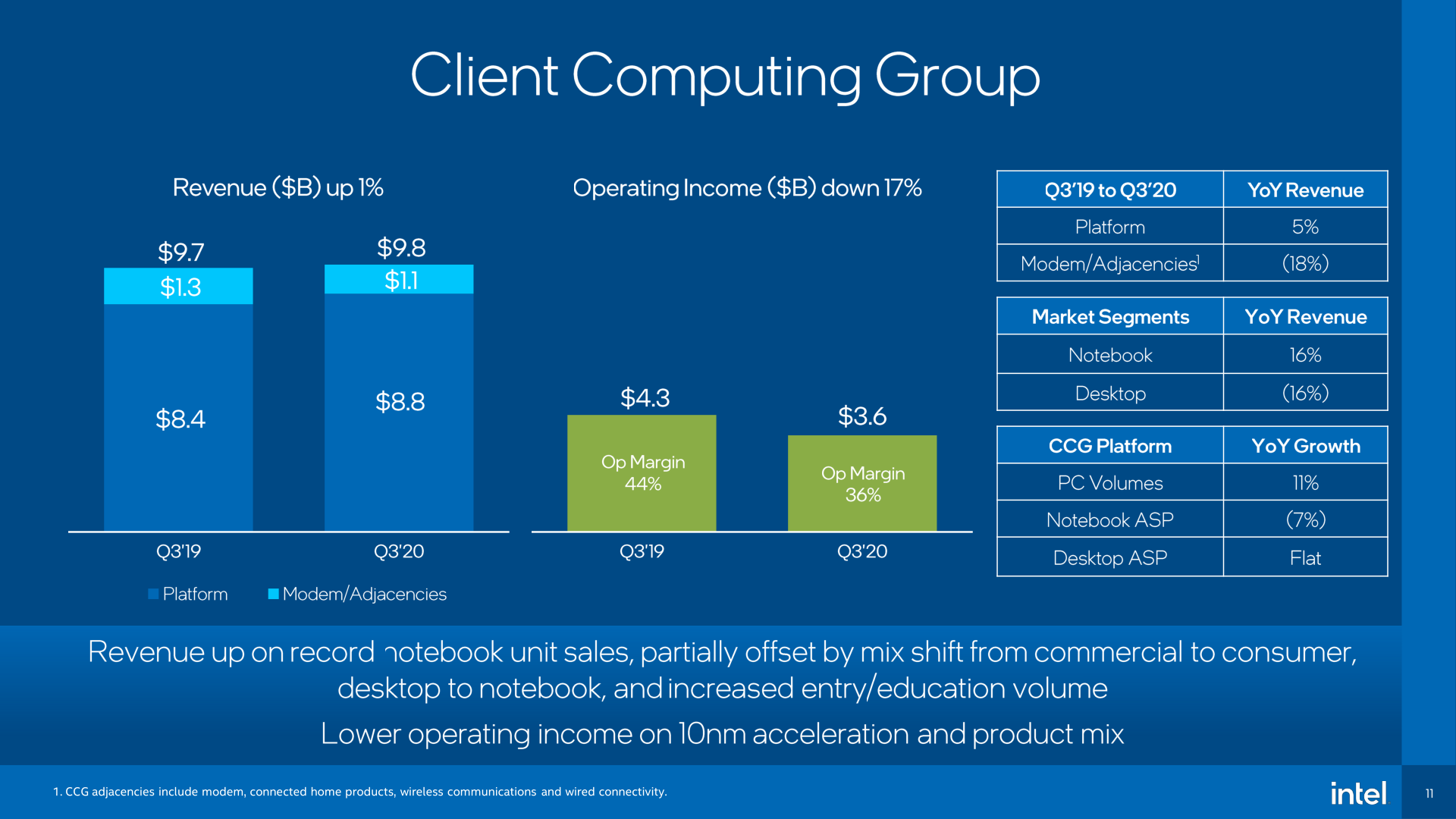

| Client Computing Group Revenue | $9.8B | +4% | +1% | ||

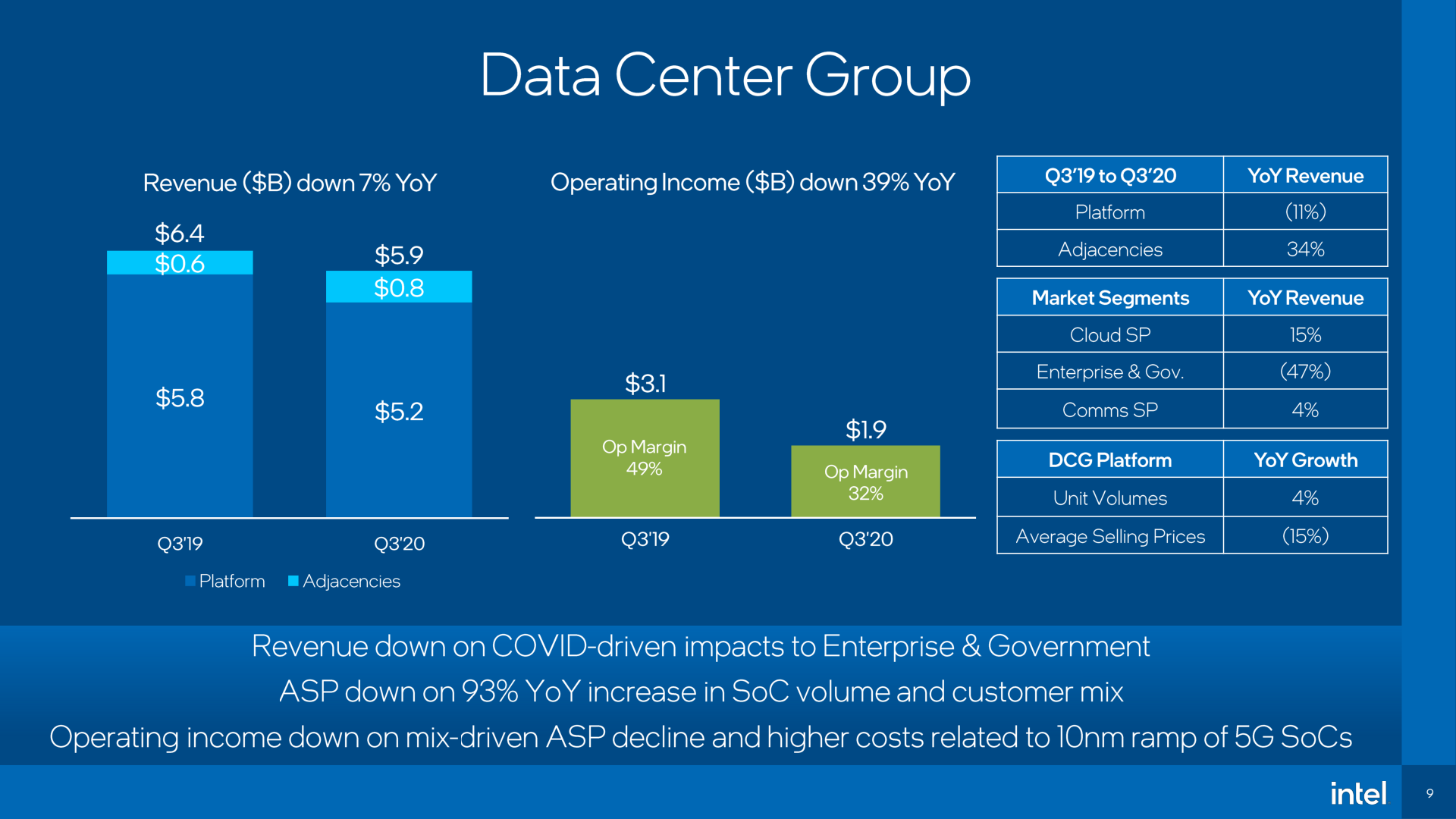

| Data Center Group Revenue | $5.9B | -17% | -8% | ||

| Internet of Things Group Revenue | $677M | +1% | -33% | ||

| Mobileye Revenue | $234M | +60% | +2% | ||

| Non-Volatile Memory Solutions Group | $1.2B | -31% | -11% | ||

| Programmable Solutions Group | $411M | -18% | -19% | ||

Breaking things down on a group basis, the majority of Intel’s internal reporting groups have seen revenue declines over the year-ago quarter. Though still not Intel’s largest segment, their data center group has been the company’s biggest star over the past year and a significant source of revenue. But revenues have begun slipping there, and for Q3’20 Intel booked $5.9B, which is down 8% from last year. Driving this decline has been a drop in ASPs, which dropped 15% versus the year-ago quarter. Breaking this down, Intel cites a significant drop in enterprise and government sales, coupled with a jump in 5G SoC sales that are dragging down the average.

As for Intel’s client computing group, revenues have held just slightly better than steady, growing 1% over last year. Still Intel’s largest group by revenue, client computing has been the most exposed to changes in buying habits from the coronavirus shift, which is represented in Intel’s revenue mix. Desktop sales are down and notebook sales are up; unfortunately notebook ASPs are down, handicapping the revenue gains there. Overall Intel is reporting that customers have shifted to less expensive processors, which has driven the revenue declines.

Meanwhile the biggest loser for Intel in Q3 has been their IoT group, which saw a 33% drop in revenue as Intel was impacted by both the pandemic and new US government export restrictions. Its counterpart Mobileye fared better, however, with revenue growing 2%.

Finally, Intel’s Non-Volatile Memory Solutions Group has been a hot topic this week, and is so again today. The group, which covers Intel’s NAND and Optane businesses, saw its revenue decline 11% versus Q3’19. According to the company ASPs are up versus this time last year, but not enough to cover a decline in total volume.

The marginally profitable group is about to undergo a split, as Intel slices out the NAND side of the business and, pending government approval, sells it to SK Hynix. The unstable, commodity nature of NAND has vexed Intel in recent years, so the company is letting go of the business in order to focus on more profitable opportunities elsewhere. Still, Intel won’t be fully divested of the business until 2025, so it will remain a part of Intel for years to come. In the meantime, the company had very little to add about the transaction in today’s earnings announcement; since Intel is the seller, the initiative to discuss the deal lies with the buyer, SK Hynix.

Overall, Q3 marked another very profitable quarter for Intel. But it’s also clear that the company is going to face some new and recurring challenges over the coming quarters, and may not be out of the woods until 2023, if not later. The biggest drag being their 7nm delays, which have seen Intel’s initial shipments pushed out to at least the end of 2022, if not later. These delays have also led to Intel looking at outside foundries (e.g. TSMC) to make up the difference, which will likely hurt Intel’s margins and leave the company fighting with other fab customers for supplies. For this reason Intel is still hoping to leverage its own 7nm fabs first and foremost, though the company doesn’t expect to make (or at least, report) its most critical decisions there until early 2021.

In the meantime, Intel has further ramped up its 10nm capacity (which wasn’t the original plan) in order to meet their needs over the next couple of years. According to the company, Intel now has 3 10nm fabs, following the recent addition of a 10nm fab in Arizona. As a result it has more capacity to handle 10nm products such as their recently-launched Tiger Lake CPUs, with Intel stating that they now expect to ship 30% more 10nm chips this year than their original plans from January of 2020 called for.

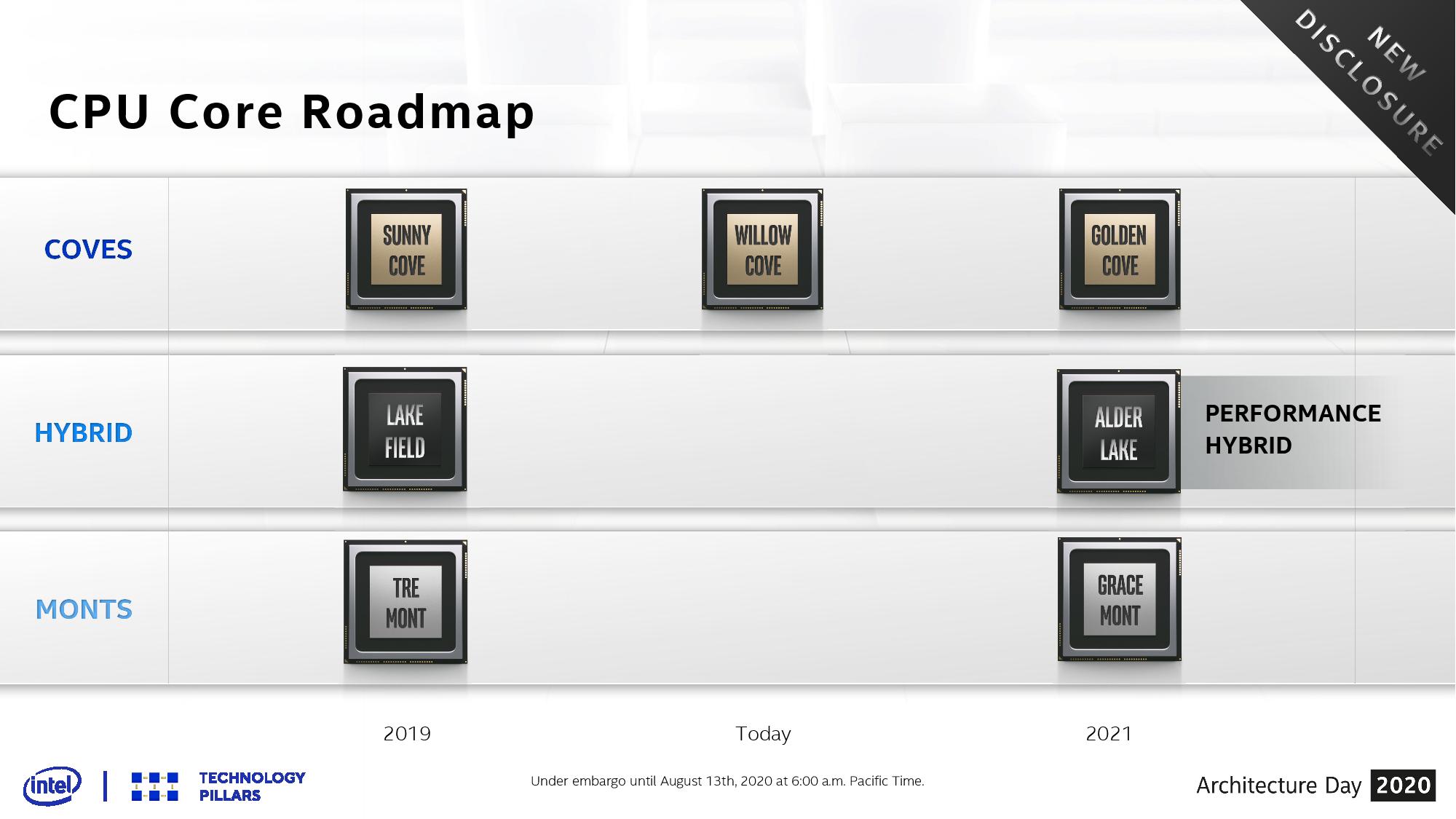

Unfortunately, Intel’s overall product mix remains in an odd spot, especially on the data center side of matters. Previously Intel has stated that Ice Lake Server (Ice Lake-SP) would start production shipments this year. And while this has technically changed, Intel has now clarified this to mean that qualification is only now taking place at the end of Q4, with volume ramps to start in 2021. Intel’s continued reliance on 14nm Skylake-based cores has been an albatross around the company’s neck, and the company badly needs a 10nm server product to improve the number of cores per CPU they can ship. However at the rate things are going, Ice Lake Server may very well end up being a short-lived part; if Intel’s Sapphire Rapids remains on schedule, the 10nm Enhanced SuperFin-based part is supposed to ship in 2021.

Speaking of future products, Intel has also confirmed that they’re now sampling Alder Lake, which will be their 2021 client CPU. Intel’s first x86 hybrid CPU, the company has previously said that it will be for both desktops and mobile, and it will also be built on their 10nm Enhanced SuperFin process. With that said, Intel traditionally samples new parts well in advance – especially for parts that will lead to major platform changes – so this shouldn’t be taken as a sign that Alder Lake is anything sooner than a Q3/Q4 2021 product.

In the interim, Intel is likely to face some of the stiffest competition in at least a decade, if not more. AMD and several Arm customers are eyeing Intel’s client and server market share (and associated profits) with their improved products, and while the company continues to talk up its own products, it's increasingly clear that they don't expect to be able to return to their traditional leadership position until at least 2023. So for now, with Intel still working to adapt to their newfound flexible fab strategy, combined with finally correcting a troubled 10nm process, it’s clear that after a long period of record revenues some challenging times are ahead for the company.

Source: Intel

27 Comments

View All Comments

HighTech4US - Thursday, October 22, 2020 - link

With Intel's (INTC) 10% share price cut in the extended market I have picked up a number of shares at $48.83. The dividend of 2.7% (at the $48.83 price) offers a nice income while I wait for Intel to get their act together which they will. AMD will make some hay right now but Intel will come back as they have done before.For investment purposes I feel that Intel with a PE under 10 and the 2.7% dividend will be a better investment for the next 5 years than AMD as AMD is currently priced for perfection with a PE of 155 and offers no dividend.

bji - Friday, October 23, 2020 - link

As if PEs even mean anything anymore. There is no scientific objective formula that states what a company's P/E ratio "should be". 155 is the new norm.michael2k - Friday, October 23, 2020 - link

PE is essentially risk.mdriftmeyer - Friday, October 23, 2020 - link

Then TSLA is nothing but risk with a P/E well past 1k.boozed - Saturday, October 24, 2020 - link

A lot of people are betting a lot of money that Tesla will be raking it in... eventually.mdriftmeyer - Monday, October 26, 2020 - link

And the VW Group will soon be pushing out several millions cars per year as EV only. Rivian will be a success very shortly. Mercedes has 14 products EV by mid 2021.Tesla's success is about to run out.

When Honda, Toyota and Nissan finally enter the room they'll be looking to gut Tesla's board or sell it off. That price point is ludicrous.

JKflipflop98 - Tuesday, October 27, 2020 - link

"Rivian will be a success very shortly."Don't keep up with current events, huh?

sorten - Friday, October 23, 2020 - link

P/E/G is more useful than PE, and when growth is negative you can draw fewer assumptions about what PE should be. Buying a dividend stock for a company that is temporarily down on its luck can be a solid move, as you suggest.But at the end of 2021 Intel will still be shipping 14 and 10nm CPUs while AMD is on 7 & 5nm. Apple is leaving the Intel camp for ARM, and ARM is coming for the data center business. Lots of pressure ahead.

Hifihedgehog - Friday, October 23, 2020 - link

"I wait for Intel to get their act together which they will."That is a lot to hinge your bets on. Unless they have a Conroe comeback, your waiting will be totally in vain.

alufan - Friday, October 23, 2020 - link

Amd have a direction and plan for the next 5 years and have executed the plan they shared in 2017 so far, am not so sure Intel has the same thing undoubtedly they will one day return but it may well be 7 years or more before they do, 10nm is a struggle, 7nm well lets not go there and 5nm? AMD i believe are in the advanced design stage and will release next Year, thats a mighty big mountain for Intel to climb especially with the new 5000 series appearing to be very much on top.